Social Security has been a very important component of retirement income for our nation’s retirees. By design, Social Security is coupled with private retirement savings and annuities or pensions for most Americans. In recent years, fears of this retiree social safety net and entitlement, to which almost all workers have contributed for their lifetimes, is at risk. We receive questions about social security from our older clients, our middle-aged clients and our young clients. In this blog, I answer some of these pressing questions with current information gleaned from the 2023 Annual Report from the Board of Trustees (this is the 83rd report that has been prepared) who report on the status of the Social Security Trust Funds (https://www.ssa.gov/OACT/TR/2023/)and from the Baird Wealth Planning Group.

Feel free to reach out with other questions. Baird also has a recorded webinar from a presentation that was delivered on June 21, 2023. To receive a link to this, send me a request to spalombo@rwbaird.com.

Will Social Security be there for your retirement?

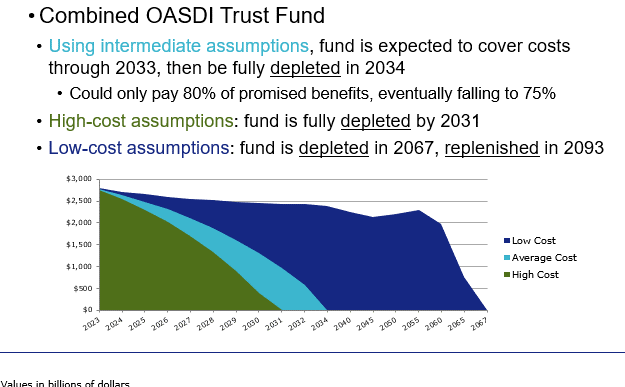

There are two separate trust funds, one is OASI (Old Age and Survivors Income-Retirement Benefits) and DI (Disability Income for disabled workers too young for OASI benefits).

The retirement benefits are projected to exceed tax and investment income every year through 2032. At the beginning of this year, the fund holds 220% of 2023 benefits. By the end of 2032, the fund is projected to hold just 7% of the projected 2033 benefits.

The disability fund has tax revenue that is expected to exceed disability benefits and the reserves continue to grow. By the end of 2032, the disability fund will hold 194% of the projected 2033 benefits compared to 77% at the beginning of this year.

The Board of Trustees Report outline potential solutions for solvency of the retirement fund for the next 75 years. They state it would require:

- Increasing the current tax rate by 3.44%, up to 15.84% OR

- Reducing benefits by 21.3% today OR

- Reducing benefits for those starting in 2021 only by 25.4%

Waiting until 2034 to address the shortfall would require:

- Increasing tax rate by 4.15%, up to 16.55% OR

- Reducing all benefits by 25.2%

Additional proposed solutions include:

- Beginning with 2024 payments reduce COLA by 1% (this would add about 5 years to solvency)

- Gradually increase FRA from age 67 to 69, delay the earliest start age from 62 to 64 by 2030 (this would have minimal impact)

- Gradually invest 40% of OASDI Trust fund in equities (assumed rate of return 5.8%) No change to solvency.

- Reduce benefits by 5% for those newly eligible for benefits in 2023 or later, no change to solvency.

- For new retirees in 2027, reduce benefits for couples with income > $120k, up to 50% reduction at $360k, no change

- Apply new 6.2% tax on investment income in 2024, similar to current 3.8% Net Investment Income Tax, this would add 4 years

- Remove the earnings cap in 2023, subjecting all earnings to 12.4% payroll tax with no credit towards benefits. (This would add 32 years to solvency)

Subject earnings >$250K to 12.4% payroll tax, with no credit towards benefits (this would add 28 years to solvency)

How can you determine your Social Security benefits?

To be eligible for social security, you need 40 quarters of earnings history to eligible for benefits.

For 2023, you earn one quarter for each $1640 of earnings. Your individual Social Security report can be found online at https://www.ssa.gov/myaccount/. If you already have an account, login. If you have not yet created an account, click on “create an account.”

The number of quarters of coverage do not impact your eventual benefits. Your benefit is based on earnings over your 35 highest-earning years. If you only worked 30 years, you will have five years of $0 years that will lower your overall benefit. The 2023 maximum creditable earnings amount is $160,200. Earnings over the annual maximum don’t impact benefits. A worker with maximum income each year would earn the maximum benefit of $3,627/month ($43,524 annually) for a 2023 retiree at Full Retirement Age (FRA).

How is social security taxed?

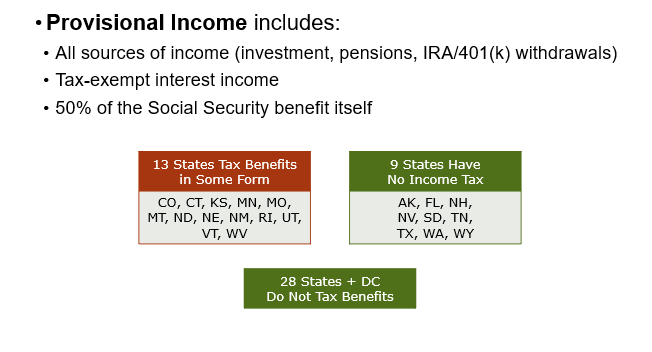

Federal taxation of social security is based upon all sources of income

Married | Single | Taxable Amount |

< $32k | <$25k | 0% |

$32-44k | $25-34k | 50% |

>$44k | >$34k | 85% |

State taxation of Social Security is dependent upon your state of domicile.

The following 13 states tax social security in some form:

CO, CT, KS, MN, MO, MT, ND, NE, NM, RI, UT, VT, WV

Nine states have no state income tax:

AK, FL, NH, NV, SD, TN, TX, WA, WY

28 states and DC do not tax benefits

When should you start benefits?

Factors to consider relative to beginning your Social Security Benefits include:

- Alternative Investment Return (Benefits increase 8%/year from FRA to age 70—can you beat that?)

- Legacy Goals-beginning SS early could preserve personal assets for legacy transfer)

- Continuing to work-social security can be reduced by employment income

- Health considerations—enjoy extra income earlier while healthy

- Maximize survivor benefit-delaying your benefit will also provide a larger survivor benefit for your spouse.

- Medicare implications—auto enrollment at age 65 when on social security, HSA considerations

- Future of Social Security solvency

- Life expectancy

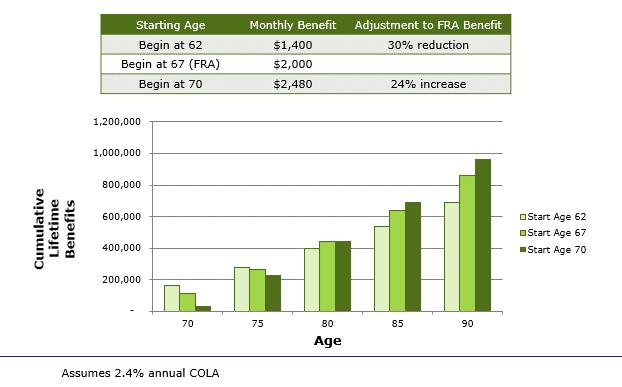

Here is one example comparing the same individual’s start date from age 62, age 67 (FRA) and age 70. The tables shows the different monthly benefits by starting age and the bar chart displays cumulative lifetime benefits at various life expectancies.

We can help with this decision. We can discuss your situation and apply tools and techniques to demonstrate the choices and implications that are available to you. We can provide a Social Security comparative benefit analysis report and update your comprehensive financial plan and look at what-if scenarios around start dates, survivor benefits, and tax implications. In addition to the social security links earlier in this blog, IRS Publication 554, Tax Guide for Seniors at www.irs.gov/pub/irs-pdf/p554.pdf and AARP Social Security Resource Center at https://www.aarp.org/retirement/social-security/

Let us know how we can help!